CND adds 341M barrels to offshore oil prospective resources

Our 2023 Energy Pick of The Year Condor Energy (ASX: CND), has just found a possible extension to its single biggest offshore oil prospect in Peru…

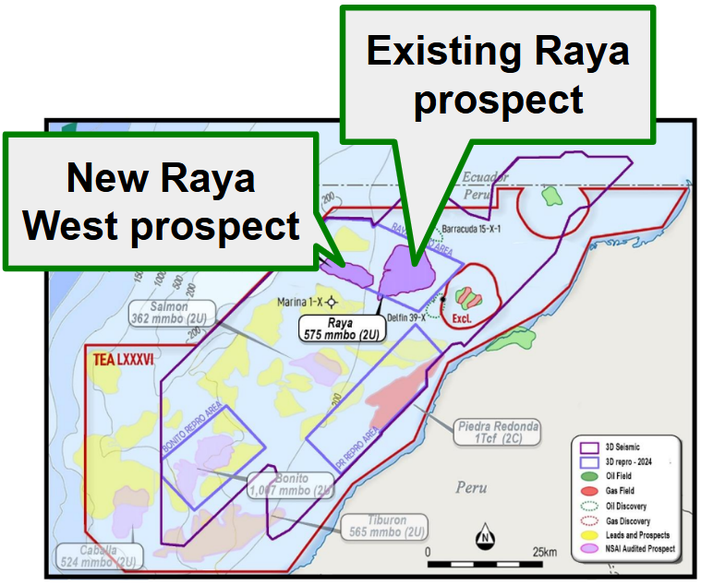

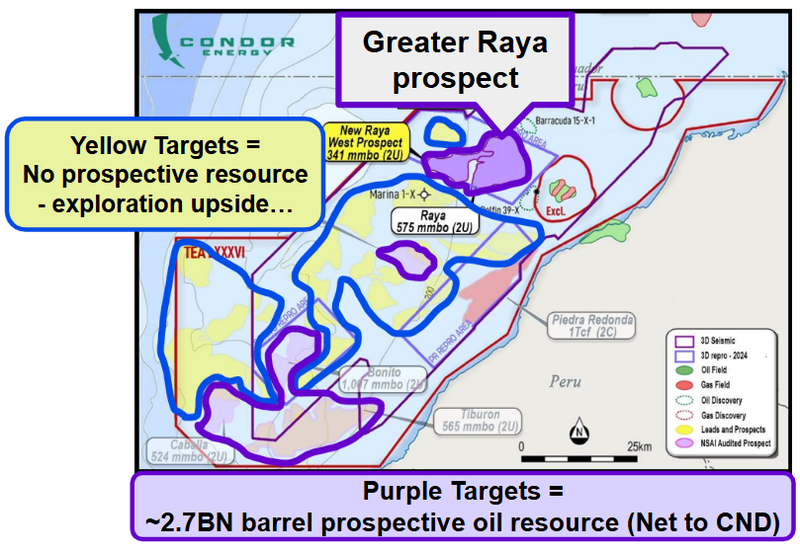

Late last year CND identified a big new structure to the west of its existing Raya prospect which on its own has a prospective resource of 575M barrels (2U gross unrisked prospective resource).

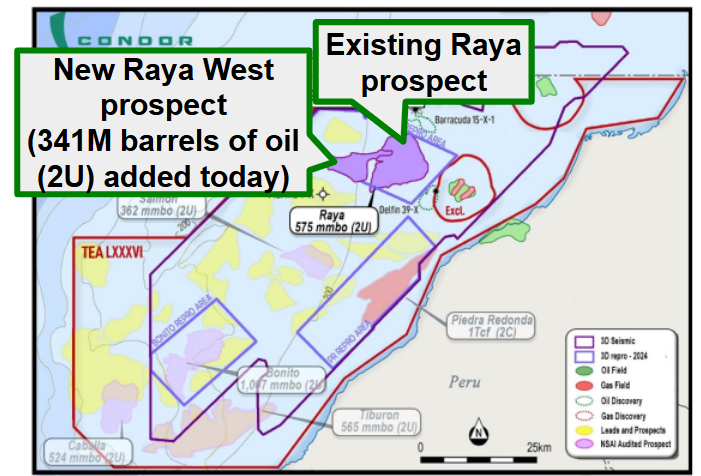

Today, by putting together the two targets, CND added a further 341M barrels to what it is now calling the “Greater Raya prospect”:

Before today:

(Source)

After the Raya West addition resource was added:

(Source)

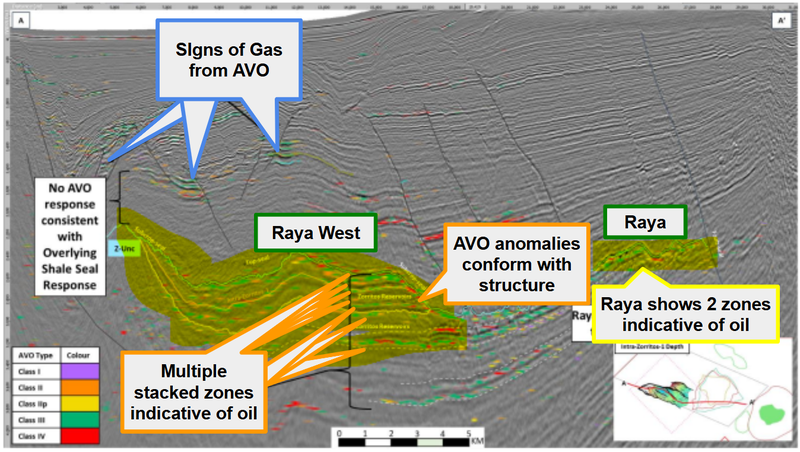

The new target was found after seismic reprocessing that showed Raya West had “multiple stacked Class II and III Amplitude Versus Offset (AVO) anomalies”.

In oil and gas exploration AVO anomalies are good early signals that targets may have hydrocarbons. Learn about AVO’s here: Lesson 27: Amplitude vs Offset

(Source)

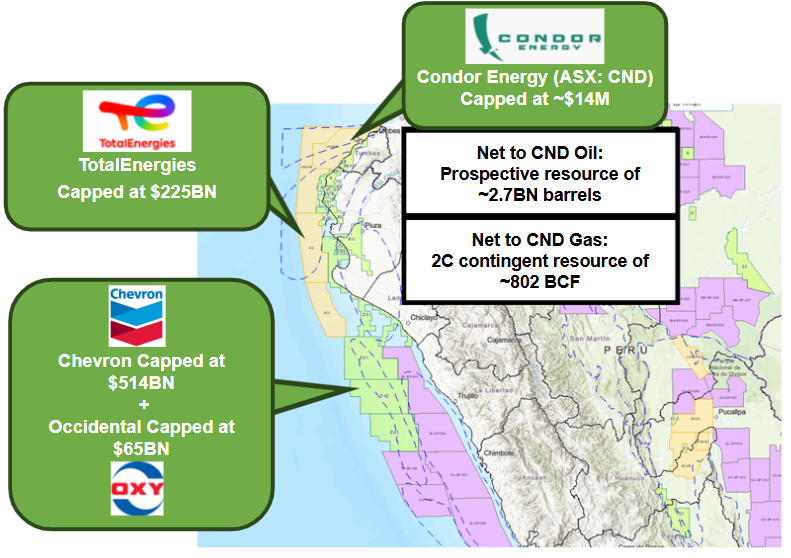

So, CND now owns 80% of a 1 Trillion Cubic Feet (Tcf) discovered gas field and more than ~3BN barrels of undrilled prospective oil resources offshore in Peru.

An area that has seen the likes of Total, Chevron and Occidental come into the region:

Is there even more exploration upside on CND’s offshore block?

At the moment CND’s asset has a ~3.3BN barrel prospective resource split across five prospects.

BUT we already know there are a bunch of leads that CND has mapped, but hasn’t put resources estimates around just yet:

(source)

We think that over time, those yellow targets could also drop into CND’s overall prospective resource numbers.

Those targets would also make for interesting exploration upside for someone looking to enter offshore Peru and secure ground that has decades of exploration upside…

When it comes to offshore oil exploration - oftentimes, major partners will only show interest in assets if they have that big untapped exploration potential - mostly due to the costs/logistical challenges of drilling offshore.

Basically, big partners want to know that the “juice is worth the squeeze”....

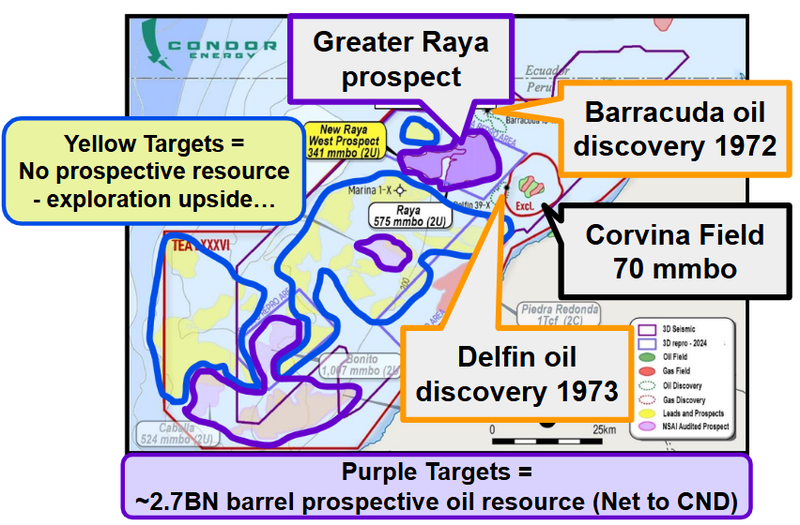

In CND’s case, we like that there is a lot of untapped exploration upside AND known oil discoveries in the same region.

There is the Barracuda oil discovery that was made in 1972 and the Delfin oil discovery made in 1973 (both of which sit inside CND’s acreage)...

AND there is the Corvina Field (excluded from CND’s block) which is currently producing oil.

CND’s most recent reports suggested it was producing ~3,000 barrels of oil per day…

The two wider basins that CND’s block sits within have produced ~1.7BN Barrels of oil historically.

So CND’s 3BN barrels in prospects that are in a part of the world where discoveries have been made and projects have been brought into production...

(source)

CND has explicitly said before that it had commenced a “Farmout process” on its block “with multiple parties in (the) data room”. (source)

We are hoping all of the above data points are enough to get a partner over the line for CND…

It’s hard to predict with so many different possibilities, but we think any of the following could be a big catalyst for CND’s share price:

- CND deals out its gas asset - maybe some of the proceeds that come from this can go toward drilling an exploration well? Maybe CND gets a free carried interest in an asset that could generate revenues in a reasonable timeframe? Now with Promigas looking at the asset, this is more in play…

- CND deals out oil exploration assets - Maybe CND gets a free carried interest in a well that would be fully funded by a farm-in partner. This means less dilution going into a big drilling event for existing shareholders…

- Maybe a combination of the two? - CND could bring someone in that is interested in both…

Occidental, Total and Chevron are all active in offshore Peru and there have been big deals happen in this part of the world before.

Back in 2009, KNOC (South Korean National Oil Corporation) and Ecopetrol (Colombian National Oil Company) signed a deal worth US$900M for projects to the south of CND’s block.

(Source)

Why we think CND is ready for a farm-out:

We think, CND is deal ready for two reasons:

- We think the oil prospects are big enough to warrant drilling AND IF someone gets lucky and discovers something there are plenty of other leads that can be followed up over CND’s blocks.

- Because a development scenario was considered for the gas asset back in 2006. Now with more demand for gas locally (in both Peru and Ecuador) as well as internationally, we think the chances someone relooks at that old development plan is much higher.

What’s next for CND?

- Volumetric analysis to calculate prospective resources for Raya West ✅ (today)

- Data room ongoing for engagement with potential JV partners 🔄